24 JUN 2026

A field guide to the creatures Masayoshi Son has summoned to explain why the numbers are fine, and to the machine that makes sure he is never the one standing in the valley.

Every empire eventually stops keeping books and starts keeping myths. You can date the transition precisely if you have the slide decks, and SoftBank has been generous enough to publish them.

What follows is a field guide to the creatures Masayoshi Son has put in front of grown adults managing pension money, each one summoned to explain why the negative number on the screen is actually a positive number wearing a disguise. There are three beasts. They arrive in order. The order is the whole story.

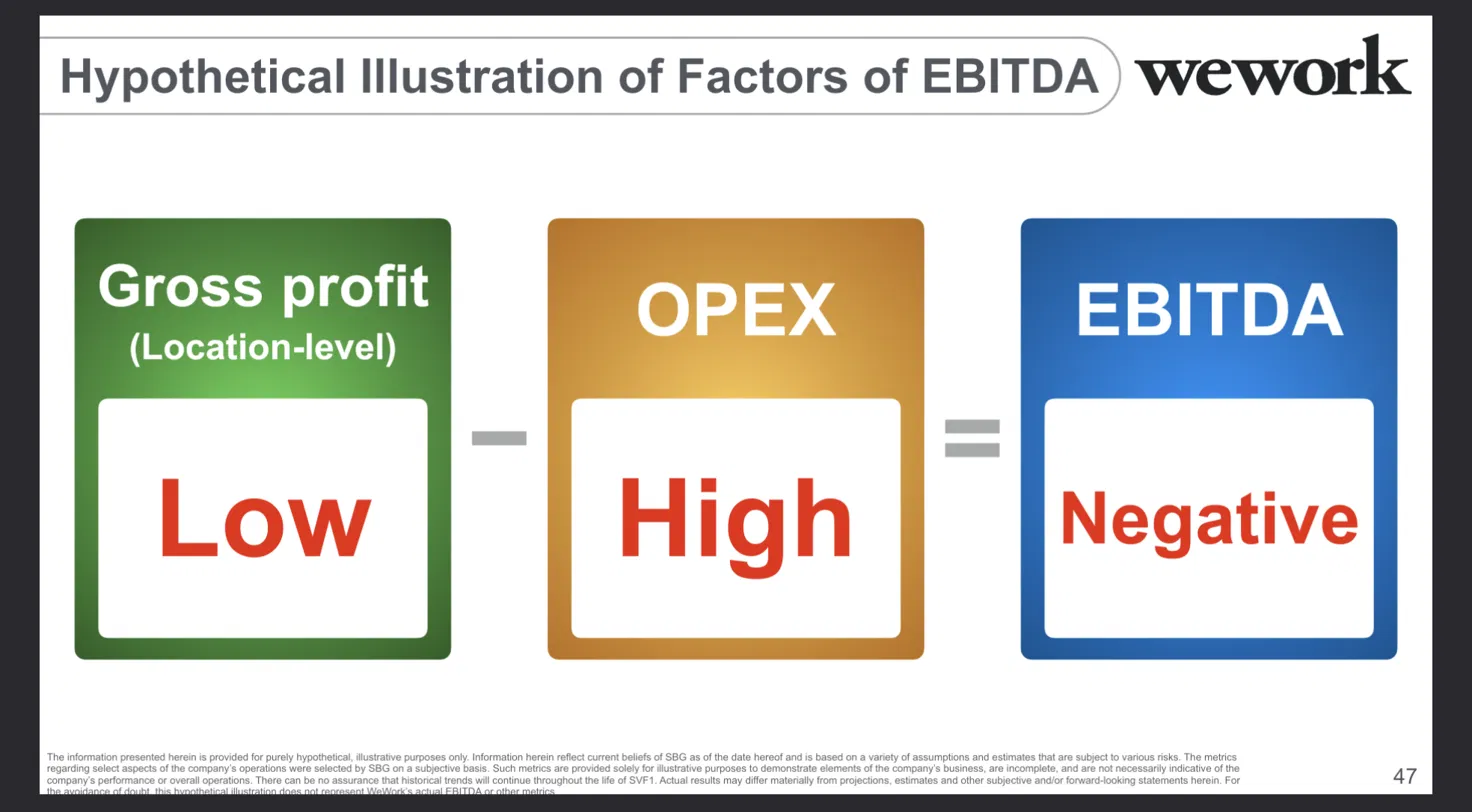

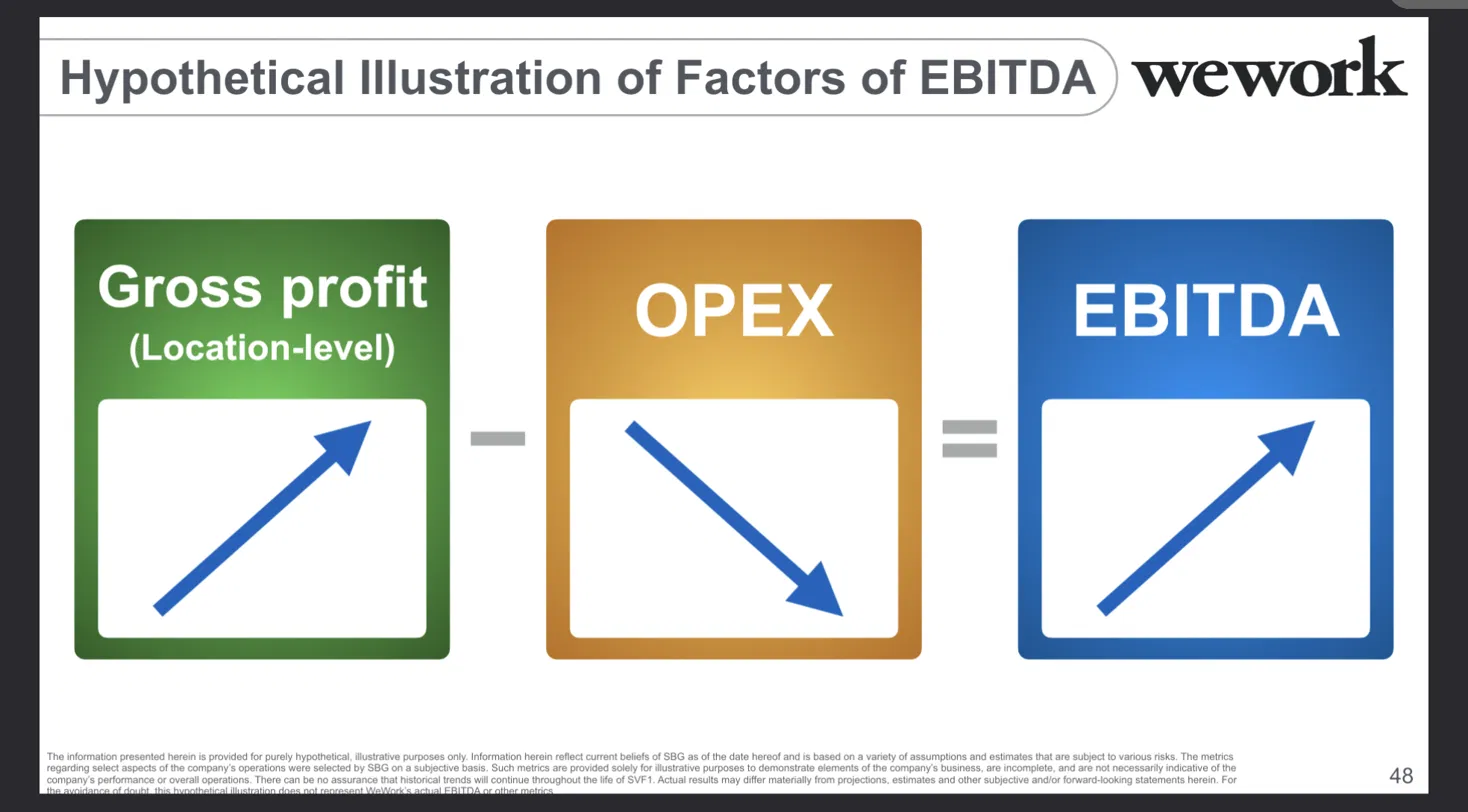

The first creature is not a creature. It is three colored boxes.

Green: gross profit, Low. Orange: operating expense, High. Blue: EBITDA, Negative. This is the Q2 FY2019 deck, the quarter SoftBank had to swallow WeWork whole after the IPO died on the launchpad. And the boxes are honest. Gross profit minus operating expense equals EBITDA is not a metaphor. It is arithmetic. A low-margin business with high fixed cost produces the oceans of negative EBITDA WeWork was producing, and the slide says so in primary colors a child could audit. Crunchbase, fact-checking the deck the next day, called the EBITDA-driver slides valid, honest, and correctly color-coded.

The mockery in 2019 landed on a different slide in the same deck, the forecast titled Hypothetical Illustration of EBITDA, a line that dives to the floor, hits a point marked "future," and then erupts up and to the right with no y-axis at all and an x-axis that runs from 0 to Future. One reader called it the year's most optimistic slide. But the box slides themselves were the responsible part of the document.

Remember this one. It is the last time SoftBank showed shareholders a true thing without a costume on it.

The boxes politely omit one fact. WeWork had by then absorbed roughly $12.8B in third-party financing across a decade, reaching a peak valuation of $47B in January 2019, the bulk of it shoveled in by SoftBank, whose all-in equity and debt exposure Reuters later totaled near $16B. The boxes explain the disease. They do not name who paid the doctor, or that by November the doctor had already written down $9.2B, about ninety percent of what he had put in.

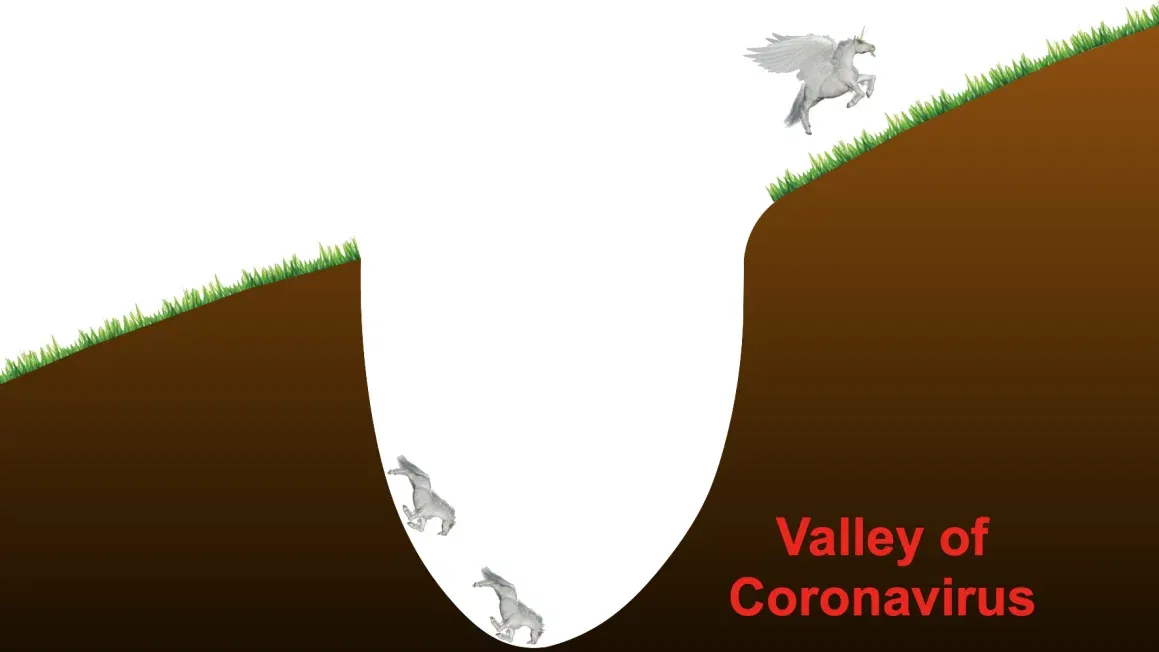

The second creature has wings.

The FY2019 full-year results were the worst SoftBank had ever printed, a net loss near $9B, with the Vision Fund alone down $17.7B. So the device was a brown chasm labeled Valley of Coronavirus with cartoon unicorns tumbling into it. On the far rim, one unicorn has grown wings and is escaping as a pegasus. The thesis, delivered without irony: some of the herd dies in the valley, some flies out the other side, and SoftBank is the kind of shepherd who can tell which is which in advance.

This is the hinge. The arithmetic is gone. In its place is a fable doing the job a chart used to do. There is still a real claim buried inside, that downturns produce survivors and casualties, but the claim now arrives as a children's book, and you are expected to invest on the strength of the illustration.

The third creature is the masterpiece.

It is a goose, rendered in service-manual cutaway, with a full industrial plant installed in its abdomen. Pipes, gauges, a robotic arm, a conveyor belt extruding golden eggs out the back. Every egg is stamped ASI. Eggs do not lay eggs, the goose lays the eggs, Son told the annual meeting, and the deck means it literally. SoftBank is the goose. The portfolio is eggs. The eggs are artificial superintelligence, which the deck defines as ten thousand times smarter than a human, and the same growth line is extrapolated to a 2042 net asset value of one quadrillion yen, roughly $6.2T. Calling any of this a bubble, Son added, is blasphemy against AI. He will not retire for at least a decade. I have become greedier, he said.

The goose is not new. Son reached for it in 2014, again in 2017, and in February 2021 he danced on the earnings stage calling SoftBank a manufacturer of golden eggs. The 2026 version simply upgraded the graphics with generative AI and bolted on a superintelligence.

Here is the trick the goose is performing, because there is a real argument inside it, the same way there was a real claim inside the pegasus. The deck puts it on a single slide as a number. Goose was not valued. Goose value 0 ? Sixteen years ago SoftBank's equity holdings were worth about ¥4.8T, net debt was ¥2T, leaving net asset value near ¥3T, and the market priced the entire company at the same ¥3T. Three eggs, valued at three eggs, with the goose thrown in for nothing. The deck now puts NAV at ¥74T as of June 23, 2026. The market still prices the whole thing closer to ¥37T. The persistent discount Son has complained about since 2014 is real, and it is enormous.

So the goose exists to deliver a defensible point. But the point now has to be reverse-engineered out of the bird's intestines, because the bird is the message and the spreadsheet is the garnish. The inversion is complete. In 2019 the chart was sober and the cartoon was a footnote. In 2026 the cartoon is the entire deck.

For twenty-two years Masayoshi Son held the world record for the largest personal financial loss in history. Guinness puts the figure at $58.6B, a fortune that ran from about $78B in February 2000 to roughly $19.4B by that July as SoftBank stock fell more than ninety percent in the dot-com collapse. Not a bad quarter. The single largest personal loss ever sustained by a human being, and he kept the title for two decades.

The record was eventually broken. The man who broke it, Elon Musk, vaporized about $182B between November 2021 and January 2023, a peak near $320B falling to $138B, and Guinness handed him the belt. This month that same man became the first trillionaire in history, crossing the line on June 12, 2026 when SpaceX went public as SPCX at $135 a share, a valuation near $1.77T, the largest IPO ever recorded.

The two people who have destroyed the most personal wealth in the history of the species are the goose-keeper and the first trillionaire.

Sit with the shape of that. One is on stage with a goose, projecting a six-trillion-dollar future and refusing to retire. The other is the richest person who has ever lived, on paper. Losing more money than anyone alive disqualified neither. At sufficient scale, it appears to be the entry requirement.

Hold the words "on paper," because they matter. Musk crossed the trillion mark for a few days and then fell back under it almost immediately. By June 21, 2026 Bloomberg marked him at $946B and Forbes at $951B, down from a peak near $1.23T on June 18. The fortune is mostly freshly public SpaceX stock he cannot sell during lockup, marked to a price the market printed for less than a week, on a company that lost $4.3B in the first quarter of 2026. The trillion was a mark-to-market artifact. So is the goose's ¥74T. Both fortunes are stories the market has agreed to believe, and both men have already demonstrated, at record-breaking scale, that the agreement can vanish in a single crash.

The reason the mythology is load-bearing, and not just embarrassing, is that the fable is what lets you raise money for a company that does not make money. You cannot put "negative EBITDA forever" on a fundraising slide. You can put a pegasus. The story is not decoration on the financial structure. The story is the financial structure, because the structure only holds if enough people accept the story in place of the books.

And the structure is built so the storyteller is never the one standing in the valley. The Vision Fund raised about $98.6B. The largest checks came from sovereign wealth: Saudi Arabia's Public Investment Fund at $45B, Abu Dhabi's Mubadala at $15B, with Apple, Foxconn, Qualcomm, Sharp, and Larry Ellison filling in. Here is the part that matters. Roughly 40% of every outside limited partner's money was structured as preferred equity carrying a 7% annual coupon, payable whether the fund won or lost, an obligation near $1.7B a year. SoftBank's own $25-28B sat in the junior common, the first-loss tranche. The outside money got a bond dressed as a venture stake. SoftBank got the downside.

This is the honest version of socialized losses. Not a taxpayer bailout, nobody from the public treasury rescued SoftBank, but a loss-distribution machine built out of a bespoke capital stack. The upside compounds to the founder and the general partner. The downside is spread across limited partners, across SoftBank's own public shareholders who eat the conglomerate discount, and across the employees of the portfolio companies who never appear on a slide. The $12.8B that went into WeWork at $47B was not Son's lunch money. When it detonated to Chapter 11 in November 2023, the people who funded the valuation ate the loss. The man who manufactured the $47B number out of a business worth a fraction of it, Adam Neumann, left with a parachute worth about $1.7B while WeWork ran layoffs. Privatized gains, distributed losses, in one resignation letter.

Look at the clearest live example, Musk's Tesla pay. In January 2024, Delaware Chancellor Kathaleen McCormick rescinded his 2018 package, a grant with a maximum value near $55.8B, finding that Musk controlled the board, that the directors who negotiated with him were not independent, and that shareholders were not honestly told what they were approving. Her question cut to the bone.

Was the plan even necessary? Swept up by the rhetoric of all upside, the board never asked the $55.8 billion question.Chancellor Kathaleen McCormick · Tornetta v. Musk · Jan 30, 2024

The system flagged the governance failure. It named it. Then it reversed itself. In December 2025 the Delaware Supreme Court overturned the remedy and restored the package, leaving the findings of control and unfairness intact but handing back the prize anyway, with $1 in nominal damages. And in November 2025, before that reversal even landed, Tesla shareholders approved a new package worth up to $1 trillion, 423.7 million shares vesting toward an $8.5T market-cap target, passed with 75% support. The penalty for being caught running a conflicted board was an upgrade.

“What you see are the eggs. What produces them is the factory itself.”

Strip the bird off and the underlying slide is the most defensible argument in any of the three decks. SoftBank does trade at roughly half its net asset value. ¥74T in assets against a ¥37T market cap. ¥13,000 of value per share against a ¥6,500 share price. Son has been right about the discount for sixteen years.

The trouble is what he wants you to conclude from it. FT Alphaville, reading the same deck the day after the meeting, put the rebuttal in the goose's own grammar.

Market cap is eggs plus goose alpha. Current goose alpha is negative.FT Alphaville · Untethered Goose Game · Jun 25, 2026

The market is not failing to see the goose. The market sees it and prices it at less than zero, because a holding company that owns volatile bets is worth less than the sum of those bets, and because the goose has spent the OpenAI windfall before it has hatched. SoftBank committed up to $40B to OpenAI in 2025, completed $41B for about eleven percent, is in talks for $30B more, and is the lead backer of the $500B Stargate project. The ¥74T is marked to this moment's enthusiasm for exactly those bets. The goose is the equity-story rationalization for the largest concentrated AI wager any single investor has ever made.

The goose is not a sign that Son has lost his mind. It is a sign that the chart stopped working and the fable did not. Twenty-six years after the largest personal loss in human history, the same man can stand in front of shareholders, point at a bird with a factory in its gut, and raise the implied valuation of the world. He can do this because the market has decided, without ever saying so, that grounded financial stewardship is a constraint for people who are not rich enough to skip it.

That is the actual mythology. Not the goose. The goose is honest by comparison. The myth is that any of this is governed.

Notes on figures. Son's 2000 loss uses the Guinness record figure of $58.6B; secondary sources cite up to $70B and stock declines of ninety to ninety-nine percent. Musk's June 2026 peak is the Bloomberg mark near $1.23T; a higher $1.4T figure circulated and is unconfirmed, so it is not used here. WeWork's $12.8B is third-party financing raised over the decade; SoftBank's all-in exposure ran closer to $16B per Reuters. "Socialization" here means distribution of losses across LPs, SoftBank's balance sheet, and minority shareholders, not a public bailout.